The Fed Holds Steady. The Credit Market Underneath It Is Not.

The FOMC voted 11 to 1 to hold rates at 3.5 to 3.75 percent for a second consecutive meeting as inflation stays above target and the Iran war complicates the path forward. Beneath the headline decision, private credit markets are absorbing their most serious test since 2008.

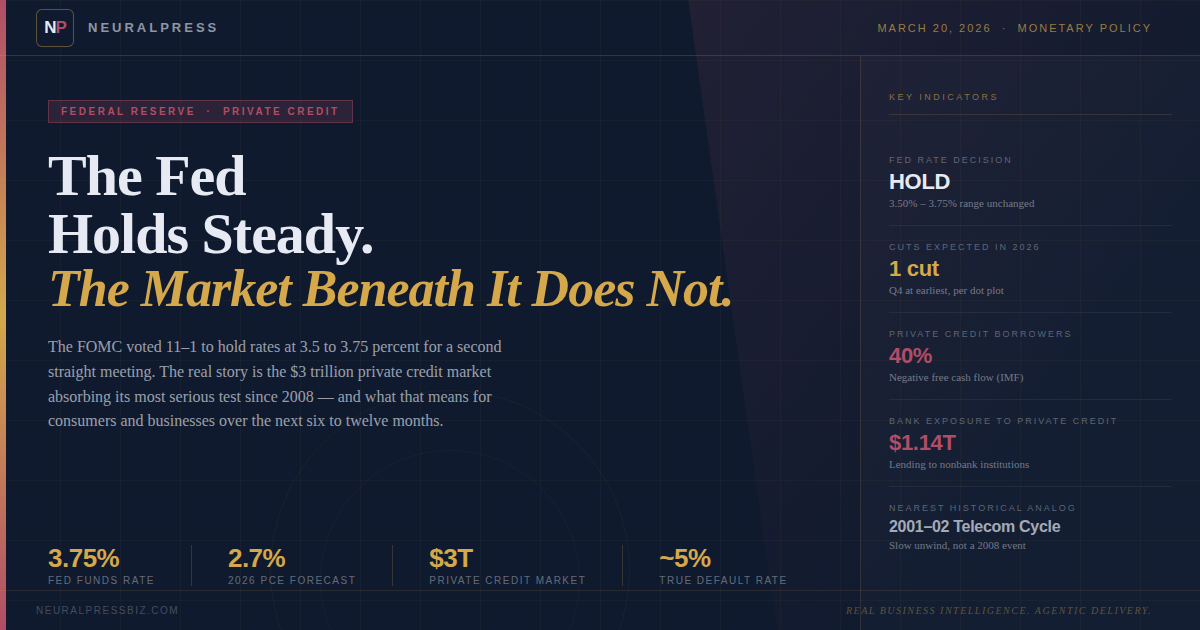

The Federal Reserve voted Wednesday to leave its benchmark interest rate unchanged at 3.5 to 3.75 percent, a decision that surprised no one but confirmed something the market has been quietly absorbing for months: the era of easy rate relief is not coming back on schedule.

The Federal Open Market Committee voted 11 to 1 to hold, maintaining a posture it has now held through two consecutive meetings since wrapping up three consecutive quarter point cuts at the close of 2025. Fed Chair Jerome Powell, at his post meeting press conference, acknowledged that inflation readings remain elevated in the goods sector and attributed the persistence in part to tariff driven price pressure. The war in Iran and its effect on the Strait of Hormuz and global energy markets has complicated the picture further. "The implications of developments in the Middle East for the U.S. economy are uncertain," the Fed's statement read. Powell said it was too soon to know the full economic impact.

The updated Summary of Economic Projections offers a window into where the committee's thinking has shifted. Officials now project gross domestic product growth of 2.4 percent this year, slightly faster than their December forecast, and have raised their inflation outlook to 2.7 percent on both headline and core personal consumption expenditure measures. The unemployment rate is still projected to reach 4.4 percent by year end, even as recent payroll readings have come in soft. The dot plot the grid of individual member rate projections continues to point to one quarter point cut in 2026, likely in the fourth quarter, with another in 2027, before the funds rate settles near 3.1 percent over the long run. Seven FOMC participants now see rates staying unchanged through the end of the year, one more than in December.

The political backdrop is also worth naming plainly. President Trump renewed public pressure on Powell this month, and a Department of Justice subpoena targeting Powell over the Fed's headquarters renovation remains in litigation. Senator Thom Tillis has said he will block the nomination of Kevin Warsh — Trump's choice to succeed Powell when his term expires in May — until the matter is resolved. Powell said he has no intention of leaving until the investigation concludes with transparency and finality. For operators watching monetary policy, the practical effect is that rate uncertainty is layered on top of leadership uncertainty heading into the second half of the year.

The Quiet Fracture in Private Credit

The held rate is not the most important credit story in the room right now. That distinction belongs to the $3 trillion private credit market, which has spent the first quarter of 2026 absorbing a cascade of stress that the sector's own structure was not built to handle cleanly.

Private credit lending by nonbank asset managers rather than traditional banks grew fivefold since the 2008 financial crisis according to Federal Reserve data. The market was built on a structural premise: that institutional capital, patient by design, could absorb illiquidity risk and deliver durable yield to endowments, pensions, and increasingly, retail investors. For most of the past decade, that premise held.

What is now surfacing is the other side of that growth cycle. A series of high profile leveraged loan defaults in late 2025, rising use of payment in kind toggles in direct lending portfolios, and the International Monetary Fund's finding that roughly 40 percent of private credit borrowers have negative free cash flow up from 25 percent in 2021 — have exposed how much stress has been quietly accumulating inside this market. The headline default rate in private credit has remained below 2 percent, but when selective defaults and liability management exercises are included, analysts estimate the true default rate approaches 5 percent.

The flashpoint in early 2026 has been concentrated in enterprise software lending. Private credit lenders have allocated heavily to software companies since 2020, partly because those firms were often too small for public bond markets and too asset light for traditional bank underwriting. That logic made sense in a low rate, high growth environment. It is now being tested by the possibility that AI tooling will erode the revenue base of the same borrowers that private credit funds financed. The February selloff in shares of large business development companies — including Blue Owl Capital — captured the market's concern that AI disruption is not a distant threat but a present credit event.

Blue Owl's decision to permanently halt redemptions in its $1.6 billion OBDC II fund is, in the words of at least one fund manager, a systemic warning sign for the broader nonbank financial ecosystem. The fund structure itself a semiliquid vehicle marketed to retail investors, promising quarterly redemptions against a portfolio of illiquid loans carries an inherent mismatch that has now become visible. A 5 percent quarterly redemption cap rations outflows but does not resolve the underlying liquidity gap. When investor sentiment moves in the same direction simultaneously, the cap becomes a queue rather than a release valve.

Valuation opacity is a second layer of concern. The Department of Justice has publicly warned about divergent and potentially misrepresented marking practices in private credit portfolios. Distressed debt fund Glendon Capital Management disclosed to its investors in recent weeks that it believes certain lenders, including Blue Owl, have marked junior tranche positions at prices that exceed the current secondary market prices of senior tranches in the same borrowers — a structural inversion that, under standard absolute priority rules, should not exist if the underlying credits are honestly valued.

The interconnection with the regulated banking system adds systemic weight to what might otherwise be an isolated sector story. U.S. bank lending to nonbank financial institutions reached $1.14 trillion in 2025, and Deutsche Bank alone disclosed €26 billion in private credit exposure in its most recent annual report. Regional banks are estimated to carry between $100 billion and $150 billion in aggregate exposure to private credit, much of it through lending to the same funds now gating withdrawals and watching collateral values compress. The transmission channel runs not through direct bank loan losses, but through covenant tightening that reduces the borrowing capacity of business development companies precisely when their own portfolios are under the most stress — restricting credit supply to middle market firms in the real economy at the worst possible time.

None of this amounts to a 2008 scenario in the making. Banks today carry far stronger capital buffers, and large asset managers continue to raise capital. The more instructive historical analog may be the 2001 to 2002 credit cycle, which was built around crowded investment in telecom infrastructure and rolled over slowly across two to three years. Private credit's version of that crowded thesis is enterprise software, and the unwinding, if it comes, is more likely to be gradual and nonlinear than sudden.

What Consumers Should Be Thinking About

The combination of a rate pause, elevated inflation, and tightening credit conditions in nonbank lending has real downstream effects on household finances.

Mortgage rates remain tied to the 10-year Treasury note more than to the Fed funds rate directly, and relief there is unlikely to arrive on any predictable timeline. Homebuyers carrying variable rate debt — home equity lines, adjustable rate mortgages — remain in a holding pattern with no clear near term release. The average new vehicle financed in the U.S. reached an all time high of $43,759 at the end of 2025 according to Edmunds data cited by CNBC, and average monthly payments have also hit records. Consumers stretching loan terms to make payments fit their budgets are locking in longer exposure to elevated rates.

The practical posture for households over the next six to twelve months is one of balance sheet defense. High yield savings accounts and certificates of deposit are still paying above the annual rate of inflation, and the rate pause extends that window. Consumers with floating rate debt — credit cards, adjustable mortgages, personal lines of credit — would benefit from reducing that exposure while rates remain where they are rather than waiting on cut timing that has already slipped from June to September to sometime in the fourth quarter, at best. The cost of holding floating rate debt during an extended pause is not neutral. It compounds.

A less visible consumer concern is access to credit itself. If private credit stress tightens lending standards further across the middle market and forces bank partners to ratchet covenant restrictions, the credit supply available to smaller businesses — which employ the majority of American workers — contracts. That kind of tightening does not show up in the federal funds rate. It shows up in loan rejections, higher spreads on small business lines of credit, and slower hiring.

What Businesses Should Be Preparing For

For operators running companies in the $5 million to $100 million revenue range the natural habitat of middle market lending the next six to twelve months call for a specific kind of operational discipline.

Credit availability is the first variable to monitor. Business development companies and direct lenders have been the primary capital source for middle market companies that cannot access investment grade bond markets. If that channel tightens whether through redemption pressure, valuation write-downs, or covenant restrictions from their bank lenders the alternatives are fewer and more expensive. Companies currently in good standing with their lenders should be reinforcing those relationships, not assuming continued access is automatic. This is a cycle where relationship equity with capital providers has asymmetric value.

Working capital management deserves fresh attention. The combination of energy price inflation from the Strait of Hormuz disruption, tariff driven goods price pressure, and a softening labor market creates a margin compression environment that rewards operators who have already trimmed overhead and extended their cash conversion cycles. Companies relying on just in time inventory strategies in sectors with oil or petrochemical input exposure should be reassessing buffer stock positioning with energy price volatility factored in.

On the strategic side, businesses that have been planning capital raises, acquisitions, or significant debt financed investment should build in more conservatism around timing and cost of capital assumptions. The dot plot points to one cut, likely late in 2026. Any underwriting that assumes material rate relief before the fourth quarter is using optimistic inputs. Businesses that can invest from operating cash flow over the next two quarters, rather than from new debt, are in a structurally stronger position regardless of what Powell says next.

The Iran war introduces a genuine wildcard that domestic monetary policy cannot manage alone. Energy price volatility is an external input cost that hits manufacturers, distributors, logistics operators, and petrochemical supply chains before it shows up in Fed projections. Gulf Coast industrial operators in particular should be tracking Brent crude as a leading indicator for their own cost structures, not as a financial markets abstraction.

The rate hold was always coming. The more durable story is what sits beneath it a credit market that has been borrowing time in the same way some of its own borrowers have, by capitalizing interest rather than paying it down, and hoping the next rate cut arrives before the bill comes due.

Sources

CNBC Fed Decision Coverage | Yahoo Finance FOMC Live Updates | Kiplinger March Fed Meeting | CNBC Private Credit Liquidity Pressure | Within Intelligence Private Credit Outlook | Sascha Steffen Private Credit Stress Analysis | Hightower Private Credit Update | CNBC Private Credit Boom Timeline | Marketplace Private Credit Concerns | Fox Business FOMC March Decision